Tuition at Cornell University for 2025 is $66K. Other top schools such as Duke, Penn, Northwestern, Stanford, or Georgetown, charge similarly. Along with additional expenses for room, board, and supplies, a 4-year degree from a leading, private institution approaches $400K.

The median household income is $80K in the United States. While scholarships are available, funding college costs also require prudent budgeting over many years. When anticipating a life-changing event such as birthing or adopting a new child occurs, consider a 529 plan. The main benefits fall into 3 categories:

- Behavioral

- Mathematical

- Structural

The Spend Less Mindset

It’s not what you make; it’s what you keep.

One drawback to drawing an allowance as a child is you spend it all when you have saved up for that one item. That works – if you have no other responsibilities. Once you begin working, funds are larger and there is more flexibility. After covering basics like rent, groceries, utilities and insurance, many (over) spend the balance of their remaining income.

It takes some discipline to build a habit of intentionally setting aside money for a savings account. To accumulate savings, at some point, you must live below your means. Setting up 529 contributions as an automatic deduction from your paycheck is periodic lump sum investing. This disciplined and simple approach achieves the timing advantage of “dollar-cost averaging” (DCA).

The premise of DCA is that investors cannot consistently time the market to buy low. From birth until high-school graduation translates to over 200 months for most students. By investing at set intervals, parents have an equal chance of purchasing investments in valleys or peaks. This approach is most suitable for long-term, multi-period investing.

As of 2024, individuals could contribute $18,000 (or couples up to $36,000) per year without triggering gift tax. DCA would dictate a $1,500 monthly investment per individual to a 529 plan. Not all are able to underwrite the maximum contribution. Start modestly – say $100 per month.

With every raise, increase contributions before upping your lifestyle. With every milestone event (calendar, religious, or academic), deposit (some) cash towards the 529 plan. Disciplined college savings plan is a behavioral shift for some. This mindset can be applied to retirement saving, eating healthy, or even exercising regularly.

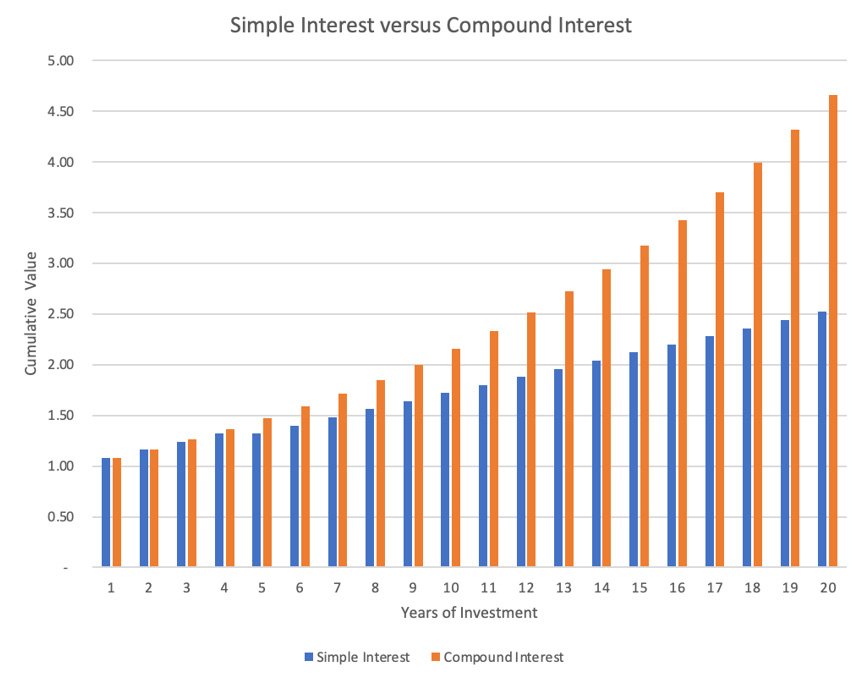

Exponential versus Linear Growth

The difference between simple and compound interest:

- Simple interest pays interest on the initial principle for each period.

- Compound interest pays interest of the initial principle as well as all accretions of interest therefrom

Assuming an 8% rate of return, where x = years invested, compound interest of 1.08^x is larger than 1*(x*.08). You may have heard the phrase “make your money work for you.” Compounding does that, in a sense.

The returns earned during year 1 could have been paid out or reinvested at the same rate as the initial investment. With continuous compounding, the rate is not 8% per year. Instead, it is 8% divided by 365 daily.

You can see that after the early years, the gap between simple and compound interest grows at an accelerating rate.

When the Government Offers Something Useful - Take It

The Internal Revenue Code passed by Congress is 7,000 pages. The number of pages balloon to 70,000 when you add explanatory notes:

- from the IRS (Internal Revenue Service) or

- settled case law.

Either way, it is a lot.

Much of the tax code is crafted by lobbyists to benefit limited, special interests. Some of the codes include carrots or sticks to promote desired behavior for ordinary citizens. Initiated in 1996, the 529 plan is one of the latter.

The 529 plan:

- offers tax-free withdrawals for qualified education expenses

- defers taxation on investment returns

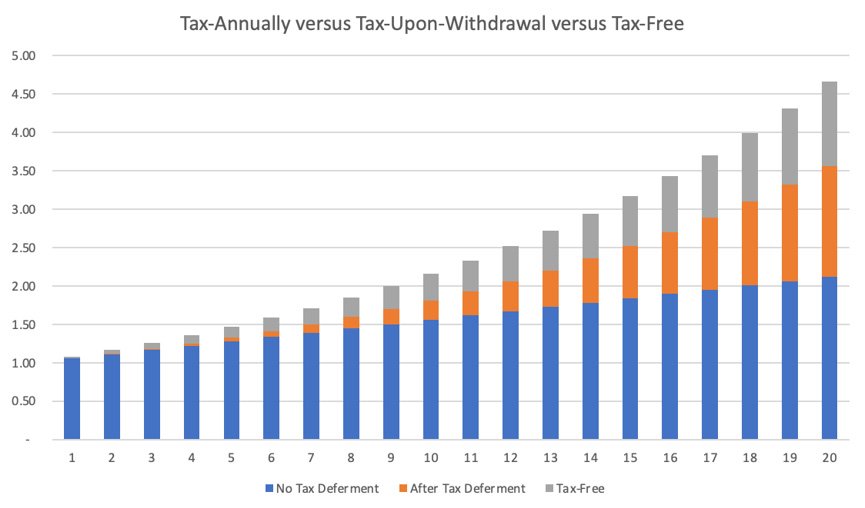

Let’s demonstrate the difference from tax deferred or tax-free where we will suppose that:

- the annual rate of return is 8%

- the individual marginal tax rate is 30%

Assuming a constant rate of return and tax rate, the table shows the projected value of $1 invested today at different points in the future, depending on the tax-treatment.

With investment returns at 8%, the accumulated balance totals $1.08 after investment earnings and $1.056 if taxed at 30%. The compound rate of return will be 1.056^x, where x is the number # of invested years. This is the series of blue bars in the graph above.

The orange section represents the benefit of tax-deferment. In other words, paying 30% tax every year from years 1 through 10 offers a lower yield compared to having a 30% tax liability only in year 10, while earning the same pre-tax investment return of 8%. Think about this as your tax liability saved in earlier years grows is reinvested with your account instead of with the government.

For tax-free withdrawals, the return will be 1.08^x, where x = years invested. This is represented as the stack of blue, orange, and gray bars in the graph above.

| End of Year | No Tax Deferment | Tax Deferment | After Tax Deferment |

|---|---|---|---|

| 1 | 1.056 | 1.080 | 1.056 |

| 2 | 1.112 | 1.166 | 1.116 |

| 3 | 1.168 | 1.260 | 1.182 |

| 4 | 1.224 | 1.360 | 1.252 |

| 5 | 1.280 | 1.469 | 1.329 |

| 6 | 1.336 | 1.587 | 1.411 |

| 7 | 1.392 | 1.714 | 1.500 |

| 8 | 1.448 | 1.851 | 1.596 |

| 9 | 1.504 | 1.999 | 1.699 |

| 10 | 1.560 | 2.159 | 1.811 |

| 11 | 1.616 | 2.332 | 1.932 |

| 12 | 1.672 | 2.518 | 2.063 |

| 13 | 1.728 | 2.720 | 2.204 |

| 14 | 1.784 | 2.937 | 2.356 |

| 15 | 1.840 | 3.172 | 2.521 |

| 16 | 1.896 | 3.426 | 2.698 |

| 17 | 1.952 | 3.700 | 2.890 |

| 18 | 2.008 | 3.996 | 3.097 |

| 19 | 2.064 | 4.316 | 3.321 |

| 20 | 2.120 | 4.661 | 3.563 |

This abstraction facilitates simple comparisons. Most investments do not have a guaranteed return rate. State tax or tax rates vary over time and by state. There might be estate planning benefits available, too. You will need to do research to develop a customized plan. Speak to a college advisor to appreciate:

- differences between going to a public versus private university,

- saving plans versus prepaid tuition

- residency requirements

- or any other specific nuances

This illustration is meant to illuminate only. Please consult your tax advisor or financial planner for more detailed information regarding your individual situation.

Beginning college at 18 might hold for many. However, a student might graduate a year early or late from High School for a variety of reasons such as health, work, or athletics. It is difficult to structure a one-size fits all solutions for families planning anticipated student expenses a couple of decades into the future. Here are some of the different features providing flexibility for 529 plans:

- You can contribute to a 529 before a child is born

- You can change the designated beneficiary

- 529 Plans can be converted to a Roth IRA, subject to federal and state income tax Roth IRA limits

- Up to $10,000 can be withdrawn for a student loan per beneficiary, beneficiary sibling or beneficiary stepsibling

- Tax-free withdrawals may include up to $20,000 in K-12 tuition per year, per beneficiary.

- No income, age, or annual contribution limits (but lifetime limit of tax-advantage contribution may vary by state)

- Most plans have no minimum contribution

You can set up an unlimited number of 529 plans, naming anyone as a beneficiary, including yourself or a friend. As an example, a grandparent can open a 529 plan in their own name years before a grandchild is born. They can change the designated beneficiary later to a grandchild. Some of the 529 college savings could be tapped for K-12 tuition expenses. If a grandchild earned a full scholarship, a portion of that “excess” savings could be allocated towards the student loan of a sibling of that grandchild or even converted to a Roth IRA for that beneficiary.

Easy Plan Management

Many plan administrators provide automated enrollment with periodic bank account withdrawal or payroll deduction. Investment options can automatically adjust based on your investment objectives or time horizon. For example, the investment setting for a 5-year-old might be more aggressive; for a 17-year-old, more conservative.

The account owner controls the funds in a 529 plan. The beneficiary has no legal rights to the funds, unless explicitly granted by the account owner. A 529 account owner can withdraw funds at any time for any reason. Non-qualified withdrawals will incur federal income tax, 10% penalty tax, and possibly state income tax, depending on the circumstances.

Financial Aid Eligibility & Estate Planning

Grandparent-owned 529 plans are not reported on the FAFSA. Parent and dependent-student 529 plan balances are considered parental assets. 2025 FAFSA standards reduce financial aid eligibility by up to 5.6% of the account’s value. While the reduction to financial aid is possible, 529 plans offer tax-free earnings when used to pay higher education expenses as well as other qualified expenses (including computers and equipment, certain K-12 tuition, or student loan repayment).

The tax benefits of a 529 plan help your account grow faster and larger and can be used for estate planning.

Special 529 rules allow a gift giver to make a lump sum contribution of up to five times the annual gift tax exclusion amount and spread it over five years (up to $190,000 for joint taxpayers in 2025).

Contributions are also subject to the amount necessary to fund qualified education expenses of the beneficiary. There are 529 plans that are prepaid tuition plans. Different states have different plans. A qualified education institution can only offer a prepaid tuition type 529 plan. A 529 plan could be used for postsecondary education as well.

It Isn’t Just for College Anymore

The specifics of 529 options change by state. The IRS often updates contribution limits, qualified expenses, tax deductions, and even eligible institutions. Review IRS sources such as:

- Tax Benefits for Education

- United States Gift (and Generation-Skipping Transfer) Tax Return.

- 2009 Expanded 529 Plan Features

- Tax Benefits for Education

The growth of tuition costs has exceeded income growth for at least the past half a century. Planning decades in advance for educational expenses involving potentially hundreds of thousands of dollars merit serious research or discussions with a CPA or Financial Planner.

As of summer 2025, 529 plan assets surpassed half a trillion dollars. While contributions are not tax deductible at the federal level, many states offer a deduction or tax credit. In addition, tax-free earnings and long-term planning appeal to many because College is expensive. The hesitancy in allocating more funds to such plans revolves around questions such as:

- What if my child does not go to college?

- What if my child’s college costs less than what is saved?

- What if I want to pursue a career in the trades that do not require college?

- What about post-college costs, such as graduate school?

- What about continuing licensing fees, courses or professional accreditations?

The latest updates in 2025 increase the scope of eligible expenses and deductible amounts. What was originally a college savings plan, has been expanded to include trade schools, continuing education, work force training, certification, and licensing programs. Both professional exams and trade certifications – including lawyers, accountants, nurses, welders, commercial drivers, or mechanics, among others – also qualify for 529 plans.

For example, the annual K-12 tuition eligible has increased from $10,000 to $20,000. Tools needed for various trades are now treated in a manner like textbooks for college. So, too, are tutoring services, including preparation for the SAT or ACT tests as well as fees for AP (Advanced Placement) college courses taken during High School.

So, keep abreast of the changing instruments, even beyond 529 plans, that can help you achieve your goals. Do not be unprepared. Get in the habit of saving regularly. The longer you can invest, the more your savings will be compounded. Take advantage of being able to use pre-tax income instead of after-tax income. Being prepared leverages resources beyond what you might have thought is possible.