In 1989, one in three American families owned stocks or mutual funds. Within a few decades, stock market participation crossed the 50% threshold of families. That democratization of stock ownership has both pros and cons.

Most evaluations emphasize the positive. We are going to point out certain dynamics in four stark terms to balance the discussion. To wit, from:

- five stakeholders to “greed is good”

- defined benefit to defined contribution

- too big to fail to too small to care

- 58% participation versus 2,700:1 distribution

Up until about the 1970s, an archetype of the American economy was:

- graduate from school, work for 1 – 3 companies during a 40+ years career

- retire with a silver watch and a pension after 25 years of service at a company

- corporations balanced the needs of five stakeholders – employees, community, customers, shareholders and suppliers

- some models included other stakeholders such as creditors or board members as distinct from shareholders, management or community

Beginning in the 1970s and accelerating thereafter came:

- corporate raiders

- leveraged buyouts

- activist shareholders

The shareholder ascended to primacy among stakeholders. Corporate independence or survival depended on placating shareholders by achieving consistent growth in revenue or earnings. Failure to efficiently make numbers would lead to investors demanding improved performance. As a result, earnings would be managed, numbers fudged, stocks repurchased, or massive restructuring, such as layoffs or outsourcing, announced to forestall a hostile takeover or boost stock prices.

The massive harm that layoffs would bestow upon employees and communities meant nothing compared to the shareholders’ benefit. The movie Wall Street reflected the “greed is good” corporate raider mentality.

After scrutinizing operating expenses, the focus shifted to the balance sheet. Among the first items considered were pensions. If overfunded, any excess was extracted. If underfunded, any excess liability was avoided or canceled. To avoid open-ended liabilities, companies began switching from defined-benefits plans to defined-contribution programs in lieu of retirement benefits.

The simplest definition:

A defined-benefit plan [or traditional pension plan] provides a specified payment amount in retirement. A defined-contribution plan [often a 401K plan] allows employees to contribute and invest in securities over time to save for retirement.

There are valid discussions concerning portability and investment awareness. A byproduct of defined contribution plans was to inject more individual capital into the stock market. Has such expanded involvement produced inflationary demand? It has certainly translated into more of the population caring about the stock market.

Corporate bailouts could be more palatably positioned as:

- saving jobs

- not destabilizing a tax base

- not hollowing out communities by having vacated commercial buildings

- preventing retirement investments from being decimated

For potentially disruptive bankruptcies, with “market-wide” implications, the Federal government embraced “too big to fail” interventions. The 2008 financial crisis froze the credit market and left many homeowners with negative equity where their mortgage exceeded their home value.

The Federal Reserve propped up issuers of toxic CDOs (collateralized debt obligations) with loan guarantees, TARP (Troubled Asset Relief Program), and printing money to buy stocks. There was no such program supporting homeowners with underwater mortgages. Homeowners were too small to care about. Did those desperate homeowners lack sufficient political clout to muster advocates?

Policies that are popularly supported are less likely to be codified into law compared to policies preferred by the concentrated wealth of the donor class. The recent study from Princeton University documents the relative irrelevance of popular support.

Does the media treat issues impacting the have nots in a way different from issues impacting the haves?

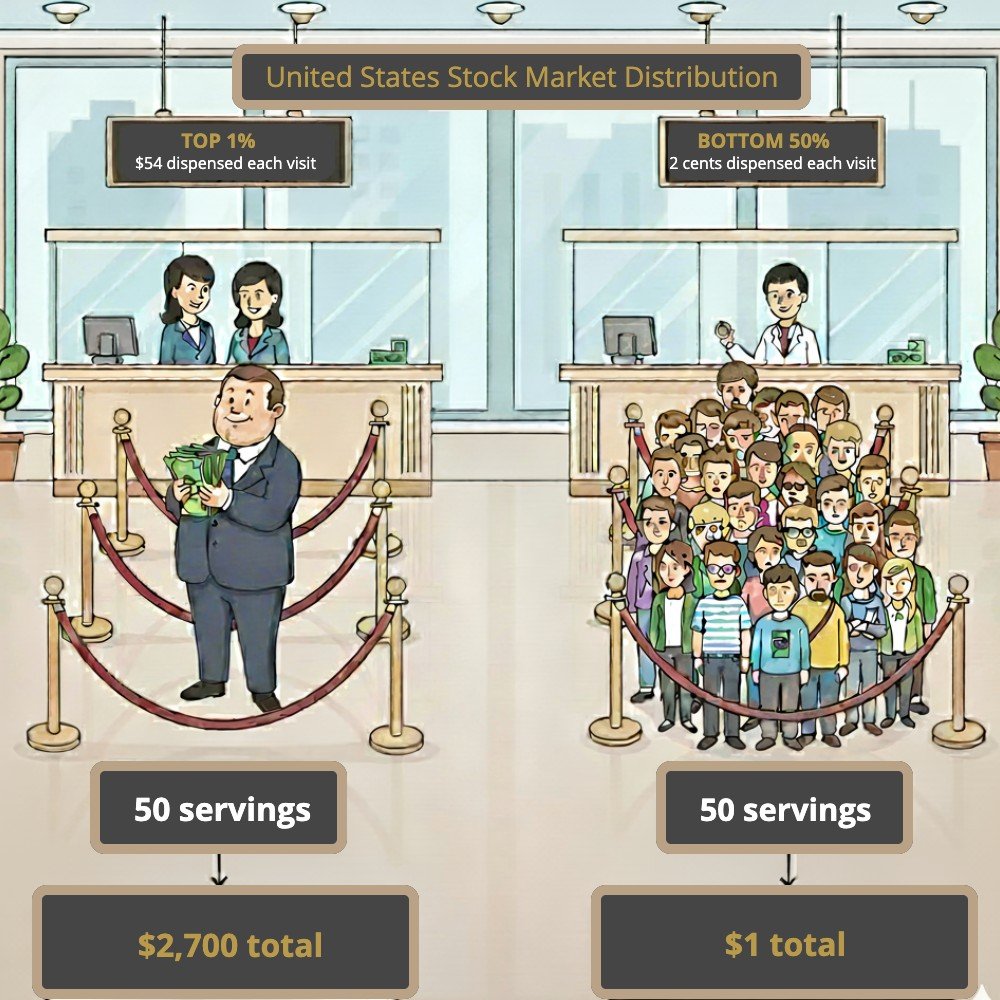

58% participation versus 2,700 to 1distribution

In 2022, the percentage of American families owning stock or mutual funds was 58%. As a result, many automatically assume what is good for the stock market is good for most Americans. Participation is important. While 58% represent the majority, the distribution of ownership confers benefits disproportionately.

In the United States, the:

| Group | Population | Equity Share | $100 Share | Per Capita |

|---|---|---|---|---|

| Top 1% | 1 | 54% | $54.00 | $54.00 |

| Top 2% to 10% | 9 | 39% | $39.00 | $4.33 |

| Top 11% to 50% | 40 | 6% | $6.00 | $0.15 |

| Bottom 50% | 50 | 1% | $1.00 | $0.02 |

| 100 | 100% | $100.00 | $ |

The first element to absorb is that the top 1% owns 54 times the stock value owned by the bottom 50%.

The bottom 50% includes 50 members for every 100 people in the population. Those 50 people share a total of $1 which calculates to 2¢ per class member.

$54 divided by $0.02 is a 2700:1 ratio!

Media coverage of policies impacting different classes

It is worth noting the way in which public policy reflexively supports the stock market without quantifying how such support is distributed among the population. Bellwether or not, should you avoid the stock market altogether or is there a way for you to be involved that makes sense for your family in the long run? There is much to consider, so we will have to revisit this topic and share more thoughts about how the media shapes opinions in additional posts.